The Era of Shopocene is fast coming to an end as high street shops are becoming a relic of the past. But high streets are not just places to shop, they’re valuble social, cultural and commercial spaces too. The Mayor must do more to protect them.

In a sci-fi novel written in the1950s, the hero survives anuclear disaster to discover a relic in an abandoned cave: a handwritten note in a coded language on a crumbling memo pad: a 20th-century shopping list.1 The novel is set in the 26th century, but it might as well be 2019: the shopping list is fast becoming a relic of another era, along with high street shops it was needed for.

Modern consumer “needs” — whether for food, household items, or contact lenses — can all now be bought online. Physical stores increasingly cater for the “wants” category. And non-vital shopping — for a new dress, say — is also often done online, perhapson an impulse triggered by an image of an influenceron Instagram. With mobile phone usage now reaching 95 per cent of those in 18-38 age bracket in the UK, soon all shoppers’ “wants” will also be capable of beingsatisfied via that shop-in-your-pocket, the smartphone.

What does this mean for London?

In London, the Era of Shopocene is fast coming to an end. The value of touching a dress in store and trying it on is massively outweighed by the minimal effort of buying a couple of dresses online with a few clicks, trying them at home and sending one back. Petrol is saved, there’s no parking hassle, and you have more time to walk the dog.

But Londoners miss their high streets, as we discovered during research on the Grimsey Reviews2; they feel depressed at seeing boarded-up shops on the way to work. High streets have social, environmental and business value beyond shopping: they provide a focal point for communities, particularly for older people, the parents of young children, and local workers. In April 2019, 400 per cent business rate increases hit many

of London’s streets even as online shopping grew by

13 per cent. Other cost increases (like the ApprenticeLevy) followed, forcing retail to give up the fight, justas we forecast it would in the Grimsey Reviews; 2018 had already seen the highest numbers of shop closure rates in retail history. A recent Centre for Cities report suggests that closures have more troubling effects for weaker high streets, which have fewer cultural amenities like cinemas, bars and gyms to sustain them after hours.3

As the new owners of House of Fraser noted, the business is not viable “even at zero rent”4; Topshop is in a similar situation.5 Shopping centres and retail parks have also seen a steep decline in footfall and spending.6It is pretty clear that London needs a high street emergency plan.

From shopping malls to social hubs

Shifting London’s high streets from traditional shopping hubs to social centres should be at the core of the new strategy, with tax support for “experience venues” like the

axe-throwing bars, escape rooms, and video-games cafesthat are now finding new audiences. No longer should webe thinking Work-Eat-Shop but, rather, Work-Eat-Play.

Londoners love events, and apps like Facebook Events, Eventbrite and MeetUp have made them much easier to promote. Zero-cost digital event invitations have made pop-up launches for new products easy to run at low cost in a way that would previously only have been affordable for big premium fashion brands.

There is a growing role for brands promoting more environmentally conscious ways of living. Two decades of cheap imports mean that most of us have more stuff at home than we have storage space – and many of us are rethinking our relationship with fast fashion,7 with younger shoppers especially wanting to support local London brands that are doing something good for the planet (or at least not making it worse). This season, ASOS, typically associated with fast fashion, has only been adding ethical brands, responding to customers’ shifting values. Landlords need to theme retail around eco-conscious shopping, ethical beauty, and vegetarian and vegan food. Londoners’ average age is 358 – only the cities of Cambridge and Oxford are younger in the UK — and millennials’ values and spending power are setting the trends in the capital.

Strength in numbers for pop-ups

New multi-brand pop-ups are beginning to appear, allowing brands to cluster and save money on rental. In Greenhaus in Shoreditch, brands share space divided into narrow display units where visitors can learn about the latest ‘green’ cocktail straw, Stroodles, try Wow You!’s vegan cosmetics, or drink coffee at the ethical coffee bar. Mixed-retail formats offer low-cost entry, with a starting package not for the whole pop-up (too pricey, thanks to near-monopoly of Appear Here) but instead a shelf or a display box, offering a chance to hundreds of new Instagram-led brands keen to show their wares in a physical space.

Mirror mirror on the wall

One online-resistant category is cosmetics. Beauty

is increasingly a cross between fashion and medical diagnostics. Clinique, for example, offers a new technology that allows customers to scan their face for a diagnosis of skin tone or damage. Staff then mix bespoke, fresh product on site and you get a moisturiser that is fresh, prepared for you, and delivered in inspiring surroundings. L’Oreal and Charlotte Tilbury offer “magic mirrors”, that let the shopper try on makeup virtually, using computervision rather than fingers, with the option to test yourchoice physically with a beauty guru in the store.

Data in the city

Boris Johnson established the London Data Portal when he was Mayor to make public data available in one place. It was a good start, but quality data about shop openings and closures are still only available from a few private sources, the best of them Local Data Company and CDRC (Consumer Data Research Centre). These organisations also supply footfall data based on Lidar sensors. Granular data, including real-time footfall, offers guidance to incoming retailers, making decisions less risky and encouraging new entrants.

A new source of retail data for London is InLinkUK, street furniture offering free public WiFi, device charging, and a screen displaying maps and ads while additionally gathering data about micro-local usage of public space. Once the base-level footfall in is established for a micro-location, the decision to take on a store and on what terms becomes more rational. This kind of data could also provide a means to evaluate business rates. Stores that generate high footfall could be incentivized with tax breaks in recognition of their contribution to the appeal of the area.

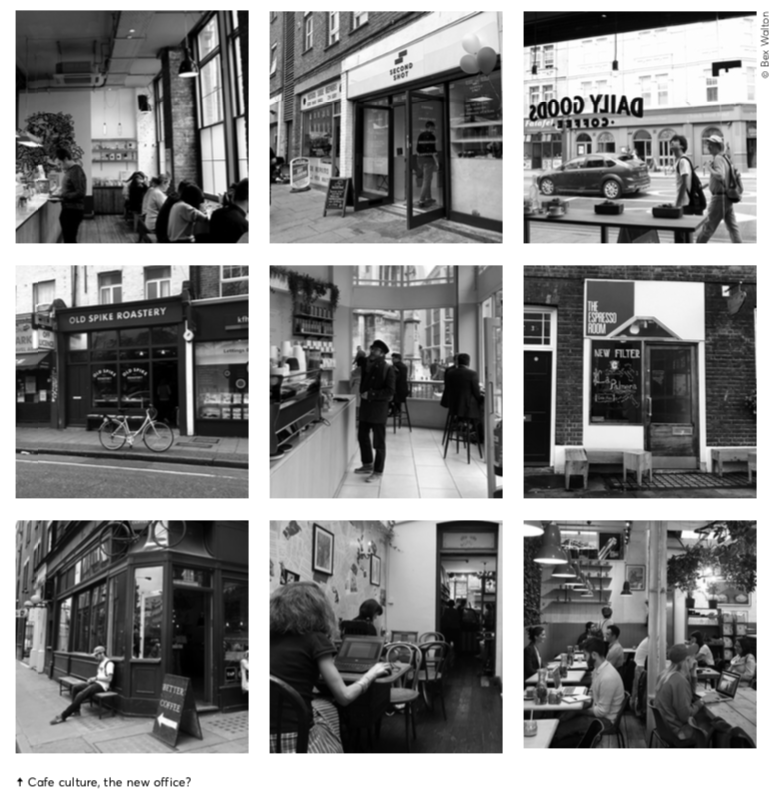

Work, eat, play

The success of co-working spaces in London indicates that the talk about working from home was largely a myth. Humans want to socialise at work, to gather around the watercooler and gossip about Bake Off. We need to support the transition to using more of London’s space for work. As London’s high streets shrink, we will have excess retail space, much of it in prime locations that could be used for work.

One use of those excess retail locations might be to convert the storefronts into advertising space for online retailers (either providing a mannequin space, or via a digital display) while using the area behind for co-working.

As the Grimsey Review 2.0 noted, we need to prioritise what people want to do on the high street. Creative mixed-use zoning will be needed to support the transition. “WeWorkVille” areas around co-working hubs are thriving by providing soft infrastructure like coffee bars, barbers, nail bars, restaurants, and clubs for those who work in the hubs.

There is limited need for new high buildings: thousands of stores exist in London which don’t need to be stores anymore but could be freed to become co- working spaces.

The capital’s planners have already supported restaurants to develop co-working during off-peak time. I frequent one, Hidden Coffee, near Camden Town Overground where my ‘quiet’ work can be done before lunch and then I can have lunch on site (much better

food than in an average co-working space). Cafe Floripa on Old Street is combining morning workspace withearly evening samba fitness lessons and a Brazilian barin the evenings.

The creative use of off-peak space in restaurants, along with the re-use of unwanted retail stock rooms for co-working, can bring people into the centre of the city. Those customers will then patronise food, drink and gym venues. We need to reclaim excess retail stores and re- occupy them: today, that increasingly looks to be as work hubs.

What next for London?

London is shifting from high streets as places to shop for “stuff” to city-centre social hubs for work and play (still shopping, in a way, but for fun experiences). High streets are needed for social, cultural and commercial reasons. Supporting their transition must be the Mayor’s priority.

With this in mind, London would benefit from

an emergency pro-retail transition policy, introducingflexible zoning, with more granular, sector–specific and location-specific business rates plus retail technologyinvestments to bring stores up to millennials’ screen- based expectations.

Investment in street sensors for more precise footfall gathering will support better retail decisions by givingretailers more confidence to take a bet on London locations.

Unlike Paris, London does not have a city-focused accelerator. What’s needed is a well funded dedicated London Commerce 2.0 accelerator, backing innovative young retailers and helping to pilot new urban commerce ideas. There is no shortage of ideas coming from a range of think tanks and urban innovation centres – but we don’t pursuethemproperly.TheexperienceofParisandBoston suggest that supporting new ideas pays off quickly.

Policymakers will need to look at planning forflexibility when it comes to how locations are used, lettingthe landlords experiment with what works. Bringing moreco-working hubs into non-traditional office locations willdrive footfall for local retailers.

London’s high streets need to find their mojo again.With new data sources, exciting retail technology, and helpful planning policies, there is plenty to be optimistic about. We will not miss our shopping lists, which will become ancient relics in the age of online shopping. Social high streets with experience-based venues and co-working hubs will help us readjust to the new, post- shopocene era. We need London to be shoppable, butfirst and foremost, sociable, and sympathetic to the needsof those who work, play and live here.

NOTES